What the Iran War Means for Your Money

Escalating conflict in the Middle East is sending shockwaves through energy markets, financial markets and living costs. The consequences for British households could be significant — and long-lasting.

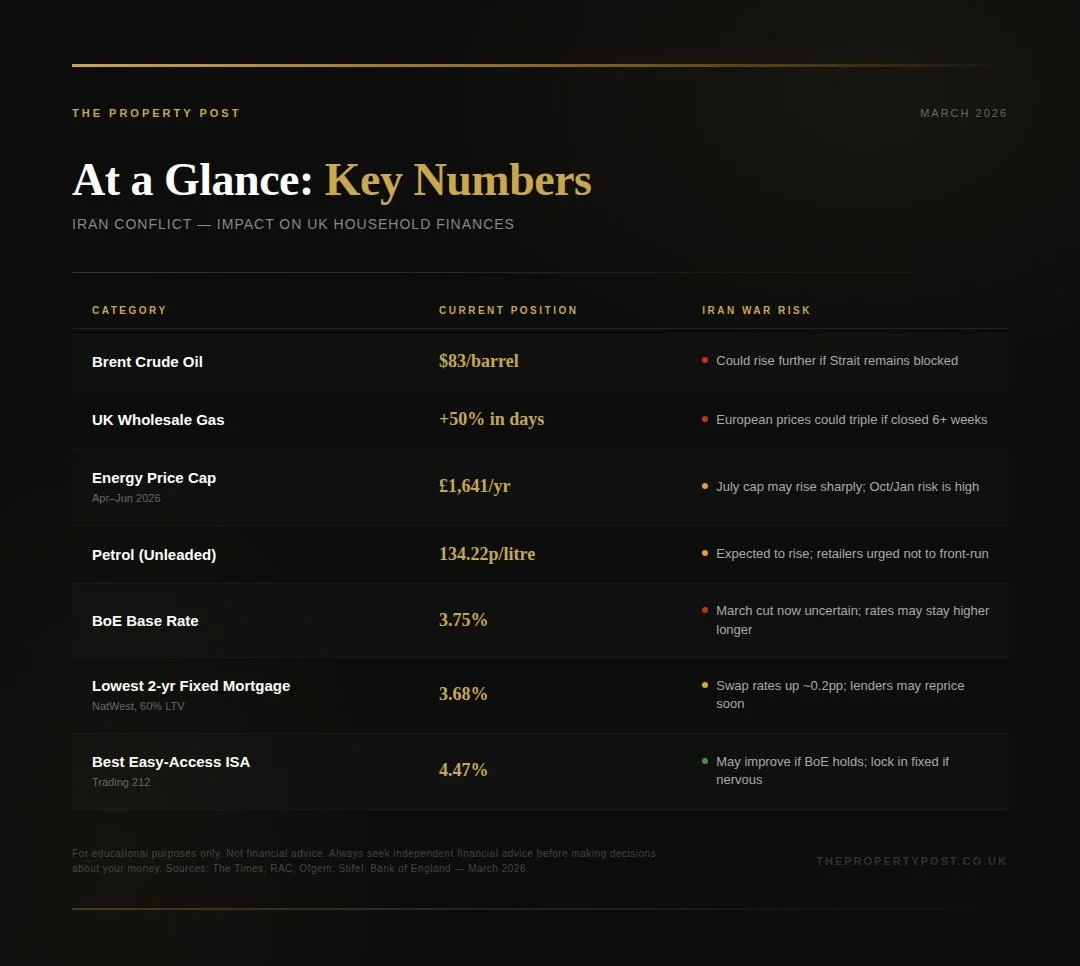

The price of Brent crude climbed above $83 a barrel in early March 2026 — its highest level in almost two years. Wholesale gas prices in the UK have spiked by as much as 50 per cent in a matter of days. Financial markets have sold off sharply. And analysts are already drawing comparisons with the energy crisis triggered by Russia's invasion of Ukraine in 2022 — an event that drove UK inflation above 11 per cent, forced the Bank of England into 14 consecutive interest rate rises, and pushed energy bills for the average household above £3,500 a year.

This time, the trigger is disruption to the Strait of Hormuz — the narrow waterway between Iran and Oman through which approximately 20 per cent of the world's crude oil supply flows every day. With traffic through the strait having almost ground to a halt, the consequences are rippling outward across every corner of the global economy.

Here is what it could mean for your household — section by section.

THE SHORT-TERM PICTURE: April brings relief — but it may not last

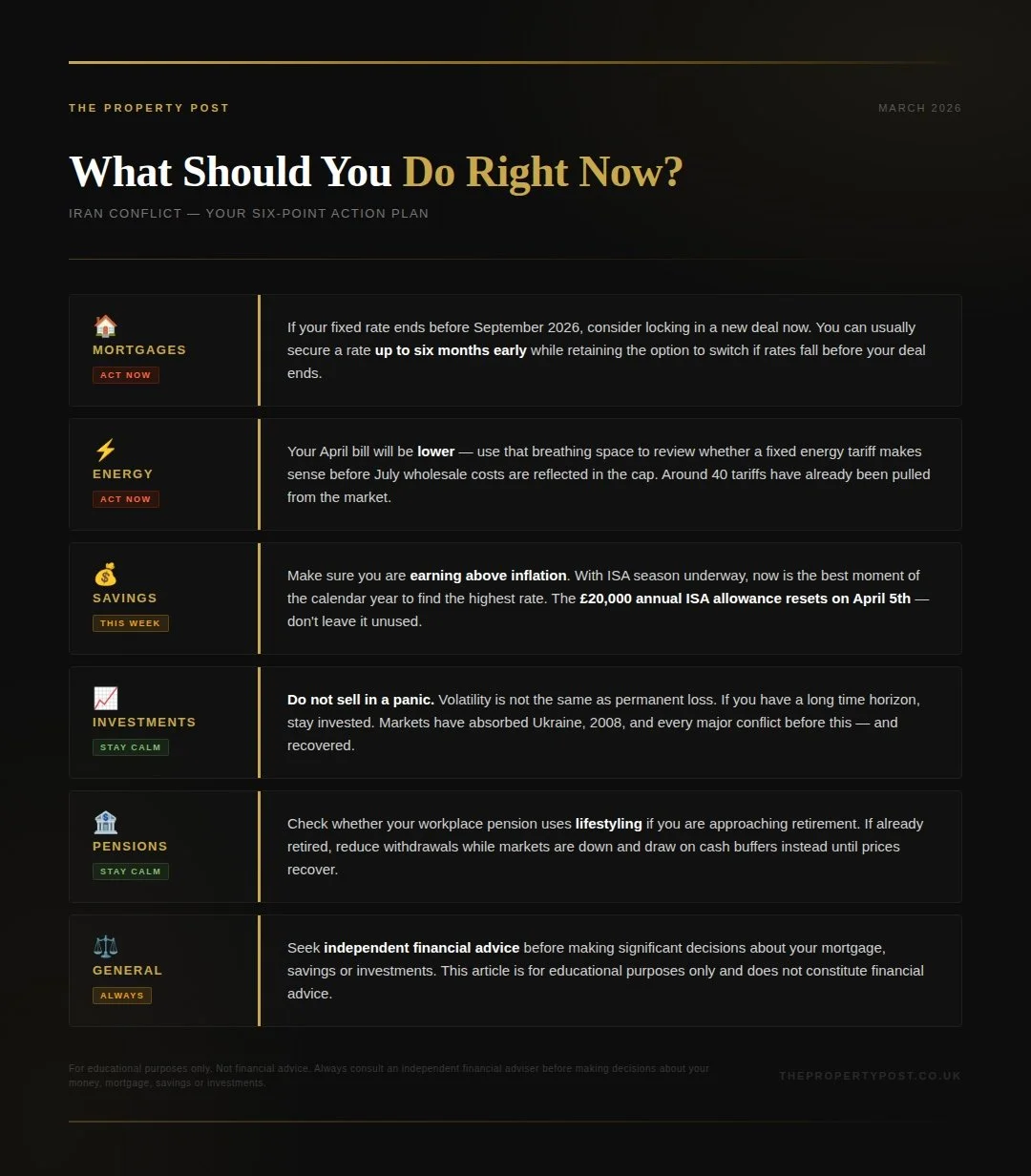

Ofgem's energy price cap for April to June 2026 has already been confirmed at £1,641 per year for the average dual-fuel household — down from the previous quarter. Every household in Britain will see their energy bill fall in April. That is the good news. The concerning news is what comes after. Higher wholesale energy costs will not be reflected in the price cap until July at the earliest. If the conflict continues and wholesale prices remain elevated, the October and January caps could rise substantially — potentially back towards levels not seen since the peak of the Ukraine crisis. Enjoy the April reduction, but do not assume it signals the end of the story.

AT A GLANCE: THE KEY NUMBERS

🛢 Petrol: Prices Are Rising — But Don't Panic-Buy

The Strait of Hormuz carries roughly one fifth of the world's crude oil. With shipping traffic through the waterway having almost ground to a halt, energy analysts are forecasting upward pressure on petrol and diesel prices at the forecourt.

As of early March 2026, the average cost of a litre of unleaded petrol stood at 134.22p, with diesel averaging 144.21p per litre, according to RAC data. Both figures are expected to rise in the coming days and weeks as higher wholesale costs filter through to filling stations.

"We really shouldn't see a shock jump in prices because wholesale fuel costs have only been rising gradually. Knowing the tendency for price increases to be passed on far more quickly than cuts, we urge retailers not to put up the price of fuel that they already have in forecourt tanks."

— Simon Williams, RAC

The Petrol Retailers Association has already written to Chancellor Rachel Reeves, asking her to abandon plans to gradually lift the 5p fuel duty cut that has been in place since 2022. That cut is scheduled to begin unwinding from September 2026. If wholesale costs are already elevated by then, the timing could not be worse for drivers.

Gordon Balmer of the Petrol Retailers Association warned that rising fuel prices feed directly into inflation — through higher transport costs for goods, higher costs for businesses, and higher household fuel bills. It is not a standalone issue; it is inflationary by nature.

⚡ Energy Bills: The April Relief Is Real — But Watch July Onwards

This is perhaps the most important section for most households to understand, so let us be clear about the mechanics.

Britain relies on gas for approximately 55 per cent of its energy. The country produces around 45 per cent of what it needs domestically and imports the rest, a small portion of which comes from Qatar — whose state energy company QatarEnergy has ceased production of liquefied natural gas (LNG) following Iranian drone attacks on its facilities.

The immediate impact on UK wholesale gas prices has been severe. Prices jumped as much as 50 per cent in a matter of days — a pace not seen since Russia invaded Ukraine in February 2022. That conflict, for context, drove the average household energy bill above £3,500 a year and triggered a national cost-of-living crisis.

"European wholesale gas prices could triple if the Strait of Hormuz was closed for more than six weeks — which could push the energy price cap back to £2,500 a year for the average household."

— Stifel, investment firm

For now, households are protected by the timing of Ofgem's price cap mechanism. The April to June 2026 cap has already been confirmed at £1,641 per year for the average dual-fuel household — which will actually mean lower bills than the previous quarter for most people. This is a genuine short-term positive.

However, the cap is reset every three months based on wholesale prices in the preceding period. Higher wholesale costs will not feed into the price cap until July at the earliest. The October 2026 and January 2027 caps represent the real risk. If the conflict continues and wholesale prices remain elevated throughout spring and summer, those later caps could rise sharply.

Laura Hinton from MoneySuperMarket reported that around 40 energy tariffs had been repriced or pulled from the market in the days immediately following the escalation. She noted that some fixed deals still offer savings against the price cap — but warned that the window to lock in may be narrowing. If you are on a variable tariff and are worried about the longer-term trajectory, it may be worth exploring whether a fixed deal makes sense for your household before rates are repriced further.

The comparison with Ukraine is instructive. In 2022, there was a window of several months between the initial price shock and the point at which household bills fully reflected wholesale costs. Those who moved early to lock in fixed deals during that window were better placed than those who waited. History may rhyme.

🏠 Mortgages: Rate Cuts Could Be Delayed — Locking In Now May Be Wise

Before the Iran conflict escalated, financial markets had been pricing in a Bank of England base rate cut in March 2026. The base rate currently stands at 3.75 per cent, and multiple cuts were anticipated over the course of 2026 as inflation had been falling steadily towards the 2 per cent target.

That picture has changed. If energy prices remain elevated and feed into inflation figures over the coming months, the Bank of England will be under far less pressure to cut — and may not cut at all in the near term. In a scenario where inflation re-accelerates, the central bank could be forced to keep rates higher for longer than anyone had anticipated even a week ago.

The mortgage market is already beginning to move. Swap rates — the benchmark that lenders use to price fixed-rate mortgage deals — have risen approximately 0.2 percentage points since the conflict began. That is a small move in isolation, but swap rates are highly sensitive to inflation expectations, and further increases are possible.

As of early March 2026, the lowest two-year fixed rate for someone remortgaging was 3.68 per cent from NatWest (available at up to 60 per cent loan-to-value with a £1,495 fee). The lowest five-year fixed rate was 3.79 per cent from First Direct at the same LTV with a £490 fee.

"We could see lenders increase mortgage rates to reflect higher swap rates, so borrowers planning to take out a fixed-rate in the next few weeks or months may wish to secure a deal now."

— Mark Harris, SPF Private Clients

Approximately 1.2 million borrowers have fixed-rate mortgage deals ending between now and September 2026. For those households, the direction of travel matters enormously. Many will have budgeted based on expectations of falling rates. A scenario where rates remain flat or tick up would add meaningful pressure to already stretched household finances.

One important note: you can typically lock in a new rate with your lender up to six months in advance, while retaining the option to switch to a better deal if rates fall before your current deal ends. In an uncertain environment, that optionality has real value.

💰 Savings: ISA Season Meets Geopolitical Uncertainty

On the surface, savers are in a relatively strong position. It is ISA season — the period before the April 5th end of the tax year when banks compete aggressively for deposits, pushing rates to their highest point of the year. The top easy-access ISA rate currently stands at 4.47 per cent from Trading 212, while the best general savings rate is 4.5 per cent from Chase (though that includes a 2.25 per cent bonus rate lasting just 12 months, so the underlying rate is lower).

For fixed-rate savers, the highest one-year rate is 4.23 per cent from Union Bank of India, while Chetwood Bank offers 4.17 per cent over two years. Virgin Money has a one-year fixed ISA at 4.15 per cent and Furness Building Society offers a two-year fixed ISA at 4.07 per cent.

The critical question is whether to fix now or wait. If the Bank of England holds rates higher for longer as a result of renewed inflationary pressure, savings rates could remain at current levels or even improve slightly. However, if you wait and the situation stabilises, you may find rates have edged downward by the time you act.

The more important principle is this: whatever rate you are earning, make sure it is above the prevailing rate of inflation in real terms. If energy price rises push inflation back above 3 or 4 per cent, a savings rate of 3 per cent is quietly eroding your purchasing power — exactly the dynamic we examined in our recent analysis of cash ISAs over the past decade.

📈 Investments: Volatility Is Not Your Enemy

Financial markets dislike uncertainty, and the initial market reaction to the escalation has reflected that. The FTSE 100 dropped sharply in the days following the outbreak of hostilities. European markets partially stabilised, but volatility is likely to persist while the geopolitical picture remains unclear.

Dan Coatsworth of AJ Bell noted that in volatile periods, investors tend to rotate toward companies with predictable, near-term earnings — insurance, utilities, food producers, household goods, and telecoms. Many of these pay dividends and represent more defensive allocations within a portfolio. They are not exciting, but in a downturn they tend to hold their value better than growth-oriented technology stocks.

In times of geopolitical stress, investors also historically move into so-called safe havens. Gold is the most traditional — and gold prices are already elevated heading into this period of uncertainty. Government bonds are another option, with the added dynamic that rising inflation expectations can push bond yields higher, which in turn can increase annuity rates for those approaching retirement.

For long-term investors, the most important thing is to resist the urge to react. Markets have absorbed major geopolitical shocks before — including the Ukraine invasion, the 2008 financial crisis, the dot-com bust, and multiple Middle East conflicts — and in each case, patient long-term investors who stayed invested recovered and continued to build wealth. Selling into a downturn locks in losses that may reverse within months.

📊 The Bigger Picture: Could This Be the Next Ukraine Shock?

It is too early to make that call with confidence. The Russia-Ukraine war of 2022 triggered a sustained, multi-year energy crisis because Russian gas had been deeply embedded in the European supply chain over decades. The Strait of Hormuz disruption is a different mechanism — a shipping bottleneck rather than a direct supplier loss — and it could ease relatively quickly if diplomatic pressure mounts or if shipping reroutes through alternative corridors.

However, the parallels are uncomfortable. In 2022, the initial shock was also described as potentially short-lived. Within weeks, it became clear it would not be. The key variable is duration. A conflict resolved in weeks has a very different outcome to one that runs for months. With approximately 750 ships backed up in the strait as of early March, according to the Chartered Institute of Procurement and Supply, the disruption is already extensive.

The inflationary transmission mechanism is well understood. Higher energy costs → higher transport and production costs → higher consumer goods prices → higher inflation → pressure on the Bank of England to keep rates elevated → higher mortgage costs and constrained household spending. Every link in that chain is now under greater stress than it was a week ago.

Whether this becomes a defining economic event for 2026 and beyond, or whether it fades as a brief episode of volatility, depends on how the conflict develops. What is clear is that the risk is real, it is material, and it is already moving prices.

DISCLAIMER: This article is produced for educational and informational purposes only.

The Property Post is not a regulated financial adviser. Nothing in this article constitutes

financial, mortgage, investment or tax advice. Past performance is not a guide to future

returns. Always consult an independent financial adviser before making decisions about

your money.